The best high yield savings account changes quickly due to high interest rates. Our instant access savings account comparison shows the offers with the highest interest rates and most attractive terms on a daily basis, based on a comprehensive assessment by reisetopia’s financial experts. We show the top 5 best instant access savings accounts in 2026!

The best high yield savings accounts in 2026

BBVA Savings account

- Promotion: 20 Euro with code BONUS

- Interest rate: 3,0% p.a.

- Interest guarantee: 6 months

- Investment amount: up to 500.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monthly

Bforbank Tagesgeld

- Interest rate: 2,5 percent p.a.

- Interest guarantee: 12 months

- Investment amount: up to 300.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: annually on 31.12

Volkswagen Bank Saving account

- Interest rate: 2,75 percent p.a.

- Interest guarantee: 6 months

- Investment amount: unlimited

- Deposit protection: 3.000.000 Euro (BdB-Fund)

- Interest distribution: monthly

Raisin StartZins Saving account

- Interest rate: 3,2 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 50.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monatlich

Norisbank Tagesgeld

- Interest rate: 3,33 percent p.a.

- Interest guarantee: until June 30, 2026

- Investment amount: up to 250.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: quarterly

The reisetopia financial experts’ comparison of instant access savings accounts is sorted according to transparent criteria. Our top recommendation offers the best current interest rate with an investment period of six months, followed by the product with the best combination of promotional and subsequent interest rates, and what we consider to be the best product currently available on the German market in terms of security.

Also in the top 5 are the best product available without a checking account and the best current promotion for new customers. All other entries are sorted according to the effective interest rate for a twelve-month investment period (promotional interest rates + regular interest rates).

Inhaltsverzeichnis

- The best high yield savings accounts in 2026

- What exactly is a high yield savings account?

- How are interest rates calculated in a instant access savings accounts comparison?

- What should you look for when comparing high yield savings accounts?

- How do I find the right product in the high yield savings accounts comparison?

- What advantages does an instant-access savings account generally have?

- What other types of instant access savings accounts are there?

- Who is an instant-access savings account suitable for?

- Do you have to pay taxes on instant access savings accounts?

- How do you open a high yield savings account?

- Conclusion on the instant access savings accounts comparison – 2026

With interest rates on the rise, the latter have become an attractive form of investment—but which is the best high yield savings account? We took a closer look at the various providers and reveal what you should definitely pay attention to when comparing instant access savings accounts.

💡 High yield savings account explained in brief

- A savings account where you invest money and receive interest in return

- Money can be withdrawn or deposited at any time

- No payment transactions take place

- Usually always free of charge

- Interest rates can vary (daily)

- No notice periods

What exactly is a high yield savings account?

Secure investments are currently more relevant than ever. Alongside checking accounts, business accounts and credit cards, instant access savings accounts are also an attractive financial tool and are proving particularly advantageous due to the interest rate turnaround.

But before you get carried away by attractive interest rates and simply take the next best offer in a high yield savings account comparison, you should first familiarize yourself with the topic of call money and clarify related terms. After all, what is a instant access savings account and how does the flow of money work?

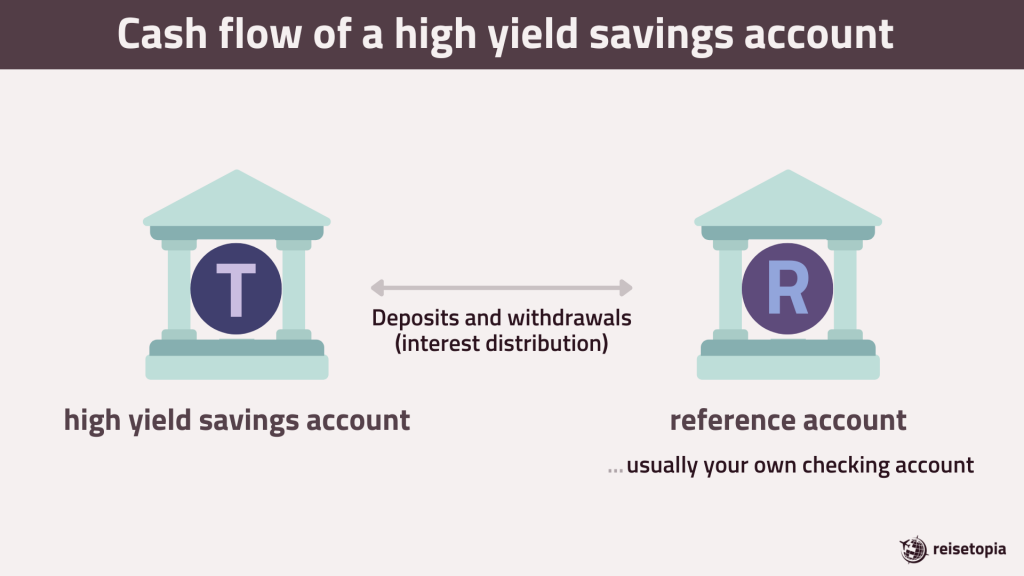

Consumers can park credit balances in the form of call money or fixed-term deposits in a so-called reference account. Such a reference account is defined as follows:

Definition of a reference account:

Unlike a checking account, for example, a reference account cannot be used for daily payment transactions. A fixed-term deposit (or time deposit) can only be invested for a specific period at a fixed interest rate.

A reference account is a special account for investing money, on which money is held but no payment transactions (such as transfers or similar) take place. Consumers receive interest on the credit balance deposited in this account.

There are no fluctuations here, as the interest rate is finalized when the fixed-term deposit account is opened. This is different from a fixed-term deposit, as a call deposit is characterized by flexibility in two respects: term and interest rate.

How are interest rates calculated in a instant access savings accounts comparison?

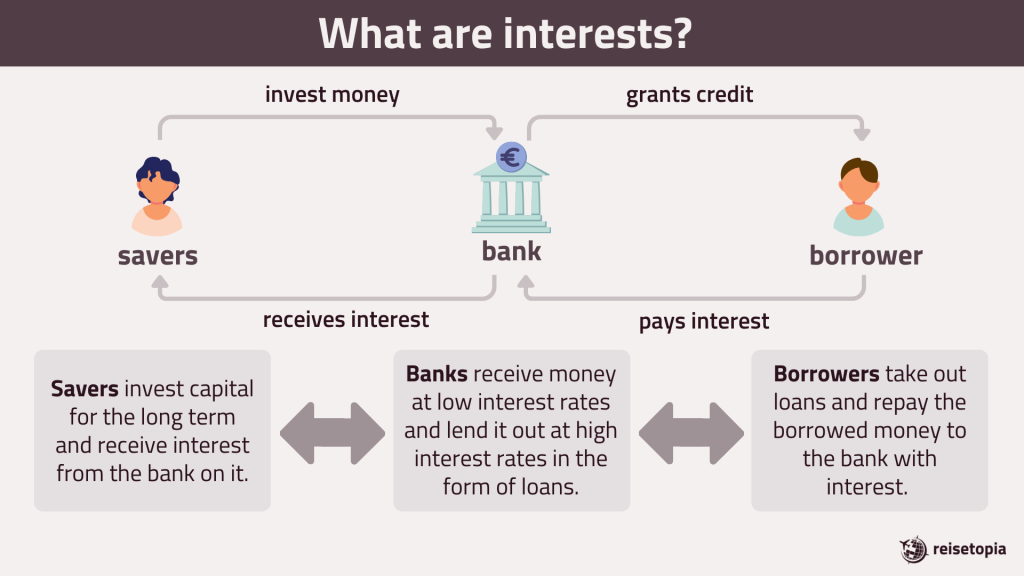

Call money interest rates are usually the decisive factor when it comes to opening a instant access savings account. However, the amount of interest charged on the deposited balance is variable and depends on the current interest rate level on the money market or the key interest rate of the European Central Bank (ECB).

This development plays a key role, because it is only in the wake of the interest rate turnaround in 2022 that the key interest rate and, consequently, the interest rates for overnight deposit accounts will continue to rise.

The interest rate for balances in an instant access savings account applies to one year (p.a.). However, this depends heavily on the provider, and in some cases there are also differences in the crediting of interest. Among other things, the interest rates offered can even vary on a daily basis, which makes it difficult to find the best high yield savings account.

In general, you should be wary of so-called lock-in interest rates, which is why the reisetopia financial experts’ overnight money comparison does not automatically put the highest-interest offer at the top of the list.

The interest rates on a high yield savings account depend on various factors, including the term, but also whether you are a new or existing customer of the bank. There are also many banks that now offer attractive interest rates on instant access savings accounts for existing customers.

Among other things, the overnight deposit rate depends on the investment amount and the selected investment term. This is because the sometimes very high advertised interest rates often only apply to new customers for a certain period of time, sometimes only a few months. In our overnight deposit comparison, this can be recognized by the so-called interest rate guarantee.

When the offer expires, the overnight interest rate falls significantly again, depending on the bank, putting existing customers at a disadvantage. Consequently, you should take a very close look at the terms and conditions for an overnight deposit account and compare providers on the basis of a long interest rate guarantee, unless you want to change your overnight deposit account regularly.

What should you look for when comparing high yield savings accounts?

Especially in a constantly changing interest rate market, it is difficult to find the best instant access savings account for your own use. That is why we, as reisetopia financial experts, also show various recommended options for each type of investment in our overnight money account comparison.

Many banks attract customers with high overnight deposit interest rates, but this should not be the only reason for opening an overnight deposit account. When assessing overnight deposit accounts, the reisetopia financial experts take various factors into account before making a recommendation.

The most important criteria in comparing instant access savings accounts:

- Interest rate

- Duration of the interest rate guarantee

- Frequency of interest payments

- Quality of deposit protection

- Minimum and maximum investment

What role does the interest rate guarantee play in overnight money?

In addition to the absolute interest rates, the interest rate guarantee for promotional interest rates also plays a decisive role in comparing instant access savings accounts. To assess this, the reisetopia financial experts therefore look at the interest rate over a period of twelve months.

This puts the interest rate guarantee, which is usually between three and six months, in relation to the subsequent interest rates. With this approach, we can give investors a meaningful recommendation that goes beyond the high interest rate at first glance.

However, thanks to our extensive database, we have also created separate comparisons for different investment periods in our overnight money comparison. This means that everyone can find the right offer based on their individual investment period.

Why is the timing of interest payments relevant?

With a call instant access savings account, the timing of interest payments plays a crucial role. As a rule, interest on call money or fixed-term deposits is credited either monthly, quarterly, or even only annually. Selected providers now even offer weekly or even daily interest payments!

The rule of thumb is that the more often interest is credited, the more attractive the account is. The so-called compound interest effect occurs because credited interest immediately starts earning interest itself.

This effect can be illustrated by an example of an investment of 10,000 Euro with an interest rate of 2 percent over a period of one and ten years with different interest intervals:

| Interest Interval | Interest Earned (1 Year) | Interest Earned (10 Years) |

|---|---|---|

| Monthly | 201.84 Euro | 2,212 Euro |

| Quarterly | 201.51 Euro | 2,208 Euro |

| Annually | 200.00 Euro | 2,190 Euro |

This shows that, for an investment over ten years, the different interest rate intervals result in a total difference of 22 Euro. The longer the investment horizon and the higher the sum, the greater the positive effect of the shortest possible interest rate interval due to compound interest.

What role does deposit protection play in reisetopia’s The reisetopia financial experts rely on a database for comparing high yield savings comparison?

Deposit protection also plays an important role in our assessment of instant access savings accounts. After all, every investor wants their invested assets to be safe. We only make recommendations if we consider the deposit protection to be sufficient.

The European Union’s statutory deposit protection provides for up to 100,000 Euro per customer at a bank to be protected. However, the location of the bank is also decisive, as there are differences in creditworthiness between countries.

In addition, selected banks offer protection for deposits of 100,000 Euro and above. That is why reisetopia distinguishes between banks with European, German, and additional German protection when comparing instant access savings accounts.

The following applies to the weighting of overnight money providers in the comparison: Banks with additional protection to German deposit protection are highlighted particularly positively, followed by banks with German deposit protection and providers with deposit protection from another country.

💡 Note: Contrary to popular belief, there is no European deposit protection scheme. Instead, deposit protection is organized nationally, but follows the same rules. This means that in all EU and EEA countries, deposits up to 100,000 Euro are protected by the respective national deposit protection scheme. It should be noted that deposit protection is provided by the respective member state, so that the actual security also depends on the creditworthiness of the national finances of each member state.

Why do we consider the minimum and maximum investment when comparing instant access savings accounts?

In some cases, high yield savings accounts require a minimum investment at a bank. In these cases, an investment is only possible from, for example, 1,000 Euro or even 5,000 Euro, meaning that the products are not suitable for everyone.

Minimum and maximum investments for overnight money have become very rare. Nevertheless, we transparently mention any restrictions in the reisetopia overnight money comparison.

In our weighting, a minimum investment is a negative factor because it excludes certain consumers. We also take a critical look at some maximum investments, especially when these are in the five-figure range.

In some cases, banks do not offer a suitable product for everyone despite active lock-in interest rates, because the particularly good interest rates are only offered for amounts up to 50,000 Euro, for example. We also take this factor into account in our detailed evaluations of all products for the overnight money comparison!

What additional conditions apply to high yield savings accounts?

In some cases, instant access savings accounts are also subject to various additional conditions. In most cases, this involves the requirement to open a checking account with the respective bank at the same time.

However, you should make sure that you can really benefit from this agreement. Unless it is an unconditionally free checking account, you should consider whether it is really worth applying for the respective overnight deposit account.

Otherwise, there is also a selection of high yield savings accounts without checking accounts. It is also worth mentioning that there are selected in instant access savings accounts that incur an administration fee. In these cases, we issue a clear warning and deduct any costs from the effectively advertised interest rate in order to provide consumers with comprehensive information.

How do I find the right product in the high yield savings accounts comparison?

Every consumer has different preferences when applying for an high yield savings account. That’s why our general instant access savings account comparison provides a transparent overview of the best high yield savings accounts currently available, based on various criteria.

However, to give you a transparent overview of the best offers for an high yield savings account, we also show the most suitable offers with different investment horizons and for different types of investors. For example, if you don’t mind changing accounts frequently, you may find an even more attractive option!

High yield savings accounts comparison with the best interest rates for 3 months in 2026

No problem with a short fixed interest period? Then the following offers in the current instant access savings account comparison are particularly exciting!

Advanzia Saving account

- Interest rate: 3,14 percent p.a.

- Interest guarantee: 3 months

- Investment amount: from 5.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monthly

Consorsbank Saving account

- Interest rate: 3,4 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 1.000.000 Euro

- Deposit protection: up to 3.000.000 Euro

- Interest distribution: quarterly

Norisbank Tagesgeld

- Interest rate: 3,33 percent p.a.

- Interest guarantee: until June 30, 2026

- Investment amount: up to 250.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: quarterly

Raisin StartZins Saving account

- Interest rate: 3,2 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 50.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monatlich

Distingo Bank Saving account

- Interest rate: 3,2 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 150.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monthly

High yield savings accounts comparison with the best interest rates for 6 months in 2026

Are high guaranteed interest rates for half a year sufficient? Then it’s worth taking a look at these providers in the instant access savings account comparison!

BBVA Savings account

- Promotion: 20 Euro with code BONUS

- Interest rate: 3,0% p.a.

- Interest guarantee: 6 months

- Investment amount: up to 500.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monthly

Volkswagen Bank Saving account

- Interest rate: 2,75 percent p.a.

- Interest guarantee: 6 months

- Investment amount: unlimited

- Deposit protection: 3.000.000 Euro (BdB-Fund)

- Interest distribution: monthly

comdirect Saving account PLUS

- Interest rate: 2,75 percent p.a.

- Interest guarantee: 6 months

- Investment amount: up to 1.000.000 Euro

- Deposit protection: 3.000.000 Euro (BdB-Fund)

- Interest distribution: quarterly

Garanti Bank Tagesgeld

- Zinssatz: 2,75 Prozent p.a.

- Zinsgarantie: 6 Monate

- Einlagensicherung: 100.000 Euro

- Zinsausschüttung: jährlich zum 31.12.

1822direkt Saving account

- Interest rate: 2,55 percent p.a.

- Interest guarantee: 6 months

- Investment amount: up to 250.000 Euro

- Deposit protection: unlimited (Sparkassen fund)

- Interest distribution: quarterly

High yield savings accounts comparison with the best interest rates for 12 months in 2026

Long-term investment horizon and no time to switch accounts frequently? Then there are many reasons to choose these providers from the instant access savings account comparison!

Scalable Capital Saving account

- Interest rate: 2,5 percent p.a.

- Interest guarantee: none (variable)

- Investment amount: flexible

- Deposit protection: 100.000 euros

- Interest distribution: monthly

Bforbank Tagesgeld

- Interest rate: 2,5 percent p.a.

- Interest guarantee: 12 months

- Investment amount: up to 300.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: annually on 31.12

BigBank Saving account

- Interest rate: 3,05 percent p.a.

- Interest guarantee: 4 months

- Investment amount: 100.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: annually

Raisin StartZins Saving account

- Interest rate: 3,2 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 50.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monatlich

Unitplus ZinsPlus

- Interest rate: 2,3 percent p.a. (after costs)

- Interest guarantee: none (variable)

- Investment amount: unlimited

- Deposit protection: unlimited

- Interest distribution: daily

High yield savings accounts comparison for accounts with additional deposit protection in 2026

Is maximum security for overnight money crucial? Then the reisetopia financial experts recommend taking a look at these overnight money offers with German and additional protection!

Unitplus ZinsPlus

- Interest rate: 2,3 percent p.a. (after costs)

- Interest guarantee: none (variable)

- Investment amount: unlimited

- Deposit protection: unlimited

- Interest distribution: daily

GEFA Bank Saving account

- Interest rate: 1,9 percent p.a.

- Interest guarantee: none (variable)

- Investment amount: up to 500.000 Euro

- Deposit protection: 3.000.000 Euro (BdB fund)

- Interest distribution: annually

Volkswagen Bank Saving account

- Interest rate: 2,75 percent p.a.

- Interest guarantee: 6 months

- Investment amount: unlimited

- Deposit protection: 3.000.000 Euro (BdB-Fund)

- Interest distribution: monthly

Hamburg Direct Bank Tagesgeld

- Zinssatz: 3,0 Prozent p.a

- Zinsgarantie: 4 Monate

- Anlagebetrag: bis 500.000 Euro

- Einlagensicherung: 100.000 Euro

- Zinsausschüttung: quartalsweise

easybank Saving account

- Interest rate: 2 percent p.a.

- Interest guarantee: 9 months

- Investment amount: up to 250.000 Euro

- Deposit protection: 3.000.000 Euro (BdB-Fund)

- Interest distribution: annually

High yield savings accounts comparison for savings accounts without a checking account in 2026

Don’t feel like getting another Schufa entry and an additional checking account? Then the following instant access savings accounts currently offer the best terms!

BigBank Saving account

- Interest rate: 3,05 percent p.a.

- Interest guarantee: 4 months

- Investment amount: 100.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: annually

Raisin StartZins Saving account

- Interest rate: 3,2 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 50.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monatlich

Unitplus ZinsPlus

- Interest rate: 2,3 percent p.a. (after costs)

- Interest guarantee: none (variable)

- Investment amount: unlimited

- Deposit protection: unlimited

- Interest distribution: daily

Suresse Savings account

- Interest rate: 3,0 percent p.a.

- Interest guarantee: 4 months

- Investment amount: up to 999.999 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monthly

Distingo Bank Saving account

- Interest rate: 3,2 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 150.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monthly

High yield savings accounts comparison with monthly or better interest payout in 2026

Want to benefit from compound interest quickly? Then these offers with monthly, weekly, or even daily interest payouts are particularly exciting!

Raisin StartZins Saving account

- Interest rate: 3,2 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 50.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monatlich

Unitplus ZinsPlus

- Interest rate: 2,3 percent p.a. (after costs)

- Interest guarantee: none (variable)

- Investment amount: unlimited

- Deposit protection: unlimited

- Interest distribution: daily

Suresse Savings account

- Interest rate: 3,0 percent p.a.

- Interest guarantee: 4 months

- Investment amount: up to 999.999 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monthly

Distingo Bank Saving account

- Interest rate: 3,2 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 150.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monthly

Openbank Saving account

- Interest rate: 1,8 – 2,2, Prozent p.a.

- Investment amount: up to 1.000.000 Euro

- Deposit protection: 100.000 Euro

- Interest payment: monthly

What advantages does an instant-access savings account generally have?

Not everyone has had an high yield savings account so far, which is why in our instant access savings comparison we also want to take a brief look at the general conditions of such an account.

These conditions apply to almost all instant-access savings accounts:

- Usually permanently free of charge

- Daily access to the balance

- Regular interest payments

- No fixed terms

Generally permanently free of charge

Unlike a checking account, you can deposit your money into an high yield savings account free of charge and do not have to expect additional fees, which may arise with regular accounts, for example in the case of inactivity.

As a rule, high yield savings accounts are free of charge regardless of whether you already have an account with a bank or open a pure instant access savings account as a new customer. However, note that in some cases a checking account at the respective bank is a prerequisite. In this case, account management fees may apply.

The reisetopia finance experts explicitly advise against high yield savings accounts that involve regular fees (either directly or indirectly via an additional checking account).

Access to the balance at any time

Another advantage of an instant access savings account is that consumers can access their balance at any time. Whether withdrawing or depositing money, funds in an instant access savings account are secure.

In addition, managing an high yield savings account is of course extremely flexible and easy to handle. With most providers, there is both an app and simple online banking.

Regular interest

Naturally, the constant interest rates also speak in favor of opening an instant access savings account. Compared to a savings book, which does not offer any advantages for new customers and nowadays usually has weak interest rates, an high yield savings account is almost always recommended.

For several months, consumers can take advantage of the effect of steadily increasing interest, at least as long as the new-customer interest rate applies. Some people choose to switch high yield savings accounts frequently in order to benefit continuously from the interest rates (also known as “interest-hopping”).

No fixed term

Another advantage of a high yield savings account is that no specific term has to be set. This differentiates the product, for example, from fixed-term deposits.

Ideally, you can also benefit from compound interest with an high yield savings account, provided the chosen bank offers monthly or quarterly payouts.

What other types of instant access savings accounts are there?

Anyone looking for the best instant access savings account will quickly realize that there are many special cases. In addition to the different investment horizons mentioned above and differences in security, there are also other special forms.

Specifically worth mentioning here are joint accounts, high yield savings accounts for corporate customers, and instant-access savings accounts for minors, each of which we have included in a separate instant access savings accounts comparison!

Instant-access savings accounts as a joint account

Holding an instant access savings account as a joint account is fundamentally an interesting way to invest money together, for example for spouses, partners, or business partners.

It offers a number of advantages and is particularly worthwhile if you want to manage or save money together.

One of the main advantages is the shared availability of the funds: both account holders can access the account flexibly, which greatly simplifies the management of joint finances, for example in a partnership or family. This is especially practical if money is to be deposited or withdrawn jointly on a regular basis.

Instant-access savings accounts for corporate customers

High yield savings accounts as business accounts offer companies several advantages. They enable flexible and secure investment of surplus liquidity reserves, as the money remains available daily. At the same time, companies can benefit from attractive interest rates without taking on the risk of long-term capital commitments.

Management of these accounts is usually straightforward, and fees generally do not apply. In addition, such accounts offer a clear separation between operational business accounts and liquid reserves, which facilitates financial planning and accounting. For companies that value liquidity and security, instant access savings accounts are an ideal addition.

Instant access savings accounts for minors

An high yield savings account account for minors is a good way to introduce children and adolescents early on to handling money and saving. Such accounts are usually opened by parents or legal guardians, as minors cannot enter into contracts themselves.

The balance remains flexibly accessible, while attractive interest rates are often offered. At the same time, minors benefit from tax advantages, as interest income up to the saver’s allowance of 1,000 euros is tax-free. These accounts are usually free of charge and give children the opportunity to develop an initial awareness of the value of money.

Who is an instant-access savings account suitable for?

An instant access savings account is primarily used to invest funds that are not needed in the short term. With an instant-access savings account, you can benefit from the interest earned without taking on significant risk, while remaining completely flexible.

Many people simply leave their money in their checking account; in the past, a savings book was often used for saving. However, compared to a high yield savings account, these two methods prove to be far less attractive, as the appealing offers in the instant access savings accounts comparison clearly show.

High yield savings accounts usually offer significantly better interest rates and have fewer restrictions than, for example, a savings book. If the saved money just sits in a checking account, you might also be more inclined to spend it faster than if it were kept in a separate account.

Such an investment can be particularly useful for unpredictable expenses or emergencies. Fundamentally, however, an high yield savings accounts is worthwhile for almost everyone, making a look at the instant access savings accounts comparison indispensable.

With regard to the very volatile interest rate environment, the reisetopia finance experts recommend regularly checking the high yield savings accounts comparison to consistently benefit from high interest rates. Often, a provider switch at least once a year is advisable for this purpose.

Do you have to pay taxes on instant access savings accounts?

Interest earned on instant access savings accounts is subject to tax, in particular the withholding tax, plus the solidarity surcharge and, if applicable, church tax. However, interest income remains tax-free up to the saver’s allowance of 1,000 Euro per person.

If earnings exceed this amount, taxes are automatically withheld by the bank, provided that no exemption order has been submitted. This automatic deduction applies only to German banks. With foreign banks, customers must take care of their tax obligations themselves.

Expert tip: When you invest money in an instant access or fixed-term deposit account, you generate investment income in the form of interest. This income is generally subject to taxation, which means that withholding tax must be paid to the tax authorities.

By submitting an exemption order to your bank, you can claim the saver’s allowance tax-free. For 2025, this allowance amounts to 1,000 Euro for single individuals and 2,000 Euro for married couples filing jointly. Any capital income exceeding this amount must be taxed at the standard withholding tax rates.

It is important to note that you must submit the exemption order yourself, which is usually possible via online banking. This saves you the effort of reclaiming overpaid capital gains tax later through your tax return.

Please note: For domestic accounts, taxes are automatically deducted at source by the bank holding the account. For foreign banks that are not based in Germany, interest income usually has to be declared and taxed independently by the account holder.

How do you open a high yield savings account?

⚠️Note: U.S. citizens or individuals subject to U.S. tax liability may face restrictions when opening savings accounts in Germany. This is primarily due to regulatory requirements such as FATCA, which create significant compliance obligations for financial institutions. Some providers – including Trade Republic – generally do not accept U.S. persons. Please check the provider’s eligibility criteria before applying.

Similar to opening a current account or applying for a credit card, an instant access savings account can be opened easily online. The process is usually quick and straightforward, as only the following information is required:

- Personal details (typically place of residence, date of birth, contact details, nationality, employment status)

- IBAN of the reference account (current account with your main bank)

- Tax identification number

- Tax residency

However, the tax identification number does not necessarily have to be provided during the initial application and can either be submitted later or obtained by the bank from the Federal Central Tax Office.

Afterwards, the information is verified either via the PostIdent procedure (identity verification at a post office) or the VideoIdent procedure (online identity verification).

When opening an instant access savings account without a current account, there is generally no SCHUFA entry. However, if the account is opened in combination with a current account, creditworthiness may play a role.

The latter option is often particularly convenient, as all that is required is a working webcam, a microphone, and a valid ID document. Once the identity check has been successfully completed, the instant access savings account is opened and funds can be transferred from the current account to the savings account immediately.

Conclusion on the instant access savings accounts comparison – 2026

Due to constantly changing interest rates, instant access savings account comparisons are highly dynamic. Thanks to an extensive database, the reisetopia finance experts have made it their mission to continuously identify the best offers and provide recommendations for the most attractive products based on transparent metrics.

Whether you are looking for the highest interest rates for a short period, a profitable long-term investment, or a particularly secure high yield savings account, our various comparisons ensure that everyone can find the perfect savings account with attractive returns.

The best instant access savings accounts in 2026

BBVA Savings account

- Promotion: 20 Euro with code BONUS

- Interest rate: 3,0% p.a.

- Interest guarantee: 6 months

- Investment amount: up to 500.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monthly

Bforbank Tagesgeld

- Interest rate: 2,5 percent p.a.

- Interest guarantee: 12 months

- Investment amount: up to 300.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: annually on 31.12

Volkswagen Bank Saving account

- Interest rate: 2,75 percent p.a.

- Interest guarantee: 6 months

- Investment amount: unlimited

- Deposit protection: 3.000.000 Euro (BdB-Fund)

- Interest distribution: monthly

Raisin StartZins Saving account

- Interest rate: 3,2 percent p.a.

- Interest guarantee: 3 months

- Investment amount: up to 50.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: monatlich

Norisbank Tagesgeld

- Interest rate: 3,33 percent p.a.

- Interest guarantee: until June 30, 2026

- Investment amount: up to 250.000 Euro

- Deposit protection: 100.000 Euro

- Interest distribution: quarterly